Selling your home? You better read this first1

FIRST THE GOOD NEWS

In June, home prices in the MetroWest region of Massachusetts reached an all-time high as most home sellers continue to receive offers in excess of their final list price.

Notably the median sales price of homes sold improved to $897,500 from $769,900 for the six months ending June 30, 2022, and 2021, respectively. This represents a 16.6% increase from the same period a year ago which is an excellent return when compared to the other asset classes (see Exhibit 1) over the same time period.

"Investments in real estate outperformed other

assets classes in the first six months of 2022."

Exhibit 1 - ASSET RETURNS (YTD JUNE 30, 2022)

| Asset Class | YTD Return |

|---|---|

| S&P 5001 | -20.58% |

| Gold Futures1 | -2.41% |

| U.S. Corporate Bonds1 | -14.39% |

| MetroWest Real Estate2 | 16.60% |

1 Source: Wall Street Journal Market Data

2 Source: MLSPIN, Domus Analytics.

This record growth in home prices primarily reflects the 1) current supply-demand imbalance in housing which still favors the seller 2) inflation expectations and 3) the likelihood that borrowing costs (i.e., mortgage rates) will continue to increase. The latter is motivating some homebuyers to submit aggressive offers, which if accepted, will enable them to avoid higher financing costs in the future.

In terms of our outlook, we renew our previous guidance that we expect home prices in the metro-west region to increase at a decreasing rate for the balance of 2022.

Beyond 2022, we expect home prices to face downward pressure from certain side-effects (see next section for details) associated with a period of high and persistent inflation.

NOW FOR THE BAD NEWS

Let’s start with a look back to how 2022 began.

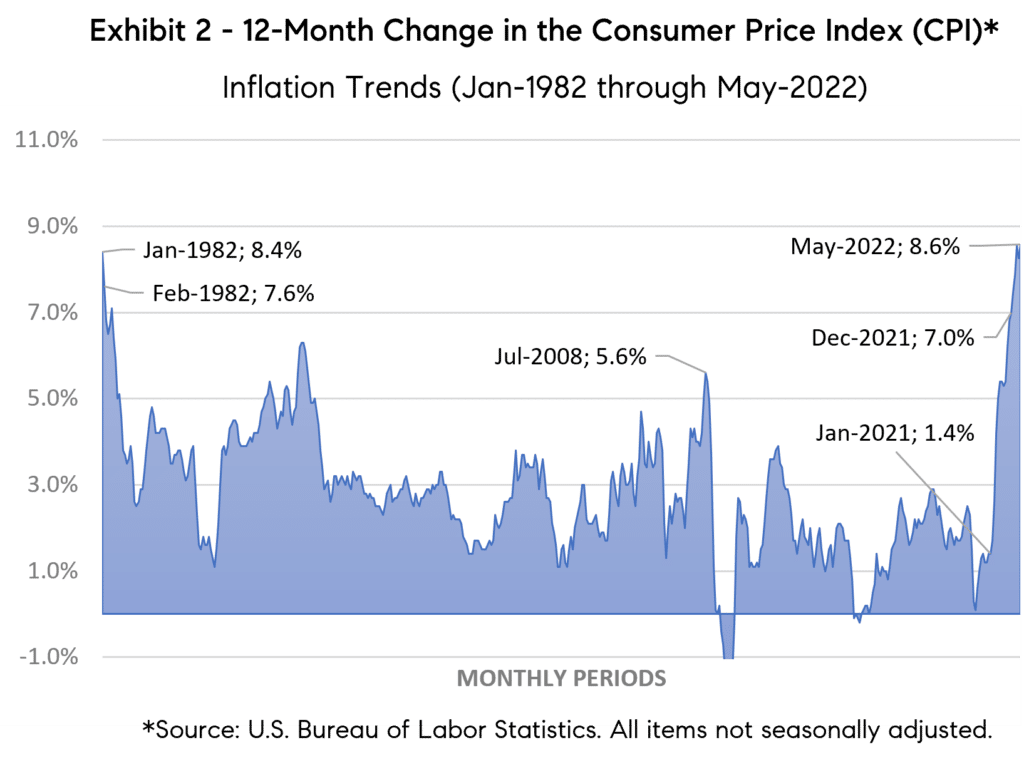

In Team Coyle’s January 2022 newsletter, we discussed how we expect inflation (see Exhibit 2), which started to emerge in the second half of 2021, to affect Massachusetts home prices in 2022.

Note, at that time, the U.S. annual inflation rate reached a forty-year high of 7% (December 2021; Source: Bureau of Labor Statistics).

In that newsletter, we stated that investments in real estate, in general, have historically proven to be an effective hedge against inflation, outperforming other asset classes (stocks and bonds – See Exhibit 1). So far that prediction has proven to be correct. However, as we noted in subsequent newsletters, periods of high and sustained inflation will produce the following four negative side effects which if not properly addressed may cause home prices to eventually decline in 2023 and beyond.

1. Higher Interest Rates

In Team Coyle’s February 2022 newsletter, we discussed why the emergence of inflation would force the Federal Reserve to aggressively respond with a series of interest rate hikes. Note the Federal Reserve uses interest rates, a key policy tool, to achieve its monetary and other goals for the U.S. economy. One of those goals is price stability or an inflation target of 2%.

At that time, we said that we expected 2022 to be another record year for home price growth in Massachusetts. However, we also said that home prices will eventually face downward pressure as higher interest rates resulting from inflation will cause long-term affordability issues for home buyers (See previous guidance in preceding paragraphs). Indeed, we are seeing that trend now.

2. Affordability and Shrinking Demand

One of the more notable long-term side effects of inflation is how it affects demand for homes.

In Team Coyle’s April 2022 newsletter, we discussed why affordability was the one issue that could derail growth in home prices. As we noted in previous blogs and newsletters, the cost of housing (both list price and financing) is becoming prohibitively more expensive especially for first time homebuyers. The net effect is a shrinking/changing level of demand for homes because homebuyers are being forced to exit the market entirely or to lower their expectations and shop for less expensive homes.

Oddly enough, inflation and these side effects may eventually cure the present supply-demand imbalance in the single-family home market. Unfortunately, the cure may occur because of a decrease in demand instead of an increase in supply. Regardless, we are beginning to see a slight shift in market leverage/advantage away from the home seller. Indeed, there has been a noticeable decline in the level of foot traffic at open houses and offers submitted/received. Moreover, we are seeing more instances of listing agents having to negotiate instead of dictate price and terms.

Affordability is Negatively

Impacting Demand for Homes

3. Recession & Unemployment

Recession = Unemployment = Lower Demand

Another side-effect of inflation is it increases the likelihood of an economic slowdown (i.e., recession) and higher unemployment.

Inflation, defined as a general increase in the cost of all goods and services in an economy, decreases the purchasing power of money for individuals and businesses alike. Consumers buy less because they can’t afford the same quantities. Businesses lower production levels to coincide with the lower level of demand. This usually results in employee layoffs as businesses need less labor to fill lower production levels. This, of course, results in an economic slowdown which if material can lead to a recession.

So how does a recession / higher unemployment affect home prices?

Generally speaking, lending institutions take a dim view of lending money to people who are unemployed (i.e., no ability to pay off loan). In other words, they don’t make good credit risks. So as unemployment rises, the pool of eligible homebuyers’ is expected to decrease. Under that scenario, it’s reasonable to assume that home prices would flatten, decline, or grow less robustly than before unemployment rose.

Similarly, if you presently own a home and become unemployed, your ability to service that monthly mortgage/home commitment may come into question. In that event, the homeowner who has no alternative source of funding may have to 1) foreclose their home or 2) sell their home prematurely and at a less favorable price then if they were gainfully employed. Either outcome is likely to place downward pressure on home prices.

4. higher property taxes

Inflation also affects the amount of property taxes a homeowner must pay to the city/township of where the home is located.

Like all enterprises, townships/cities have obligations they need to fund. These entities rely entirely on your property taxes to fund those obligations. The largest, of which, is the school budget which generally counts for the largest share of the city/town’s budget.

As inflation occurs, townships/cities, like businesses, will need to collect more revenue (taxes in this case) to fund the increase in its expenses. This will, of course, result in higher property taxes and thus a higher cost of housing for the ordinary homeowner or potential homebuyer. The implications, of which, may depress home prices in order to make total housing costs (i.e., cost of house, property taxes, finance costs, utilities, etc.) more affordable to ordinary homebuyers.

Disclaimer: The views and opinions expressed in this commentary reflect Team Coyle’s beliefs and observations as of the date of publication. Team Coyle undertakes no responsibility to advise you of any changes in the views expressed herein. No representations are made as to the accuracy of such observations and assumptions and there can be no assurances that actual events will not differ materially from those assumed. The forward-looking statements in this paper are based on Team Coyle’s current expectations, estimates, forecasts and projections, and are not guarantees of future performance. Actual results may differ materially from those expressed in these forward-looking statements, and you should not place undue reliance on any such statements. These materials are provided for informational purposes only, and under no circumstances may any information contained herein be construed as investment advice. See also terms of use.

About TEAM COYLE

Team Coyle, a professional group of real estate agents at Compass, has more than ten years of experience helping individuals and families buy and sell real estate in the Greater Boston Region of Massachusetts (primarily MetroWest).