U.S. Inflation Worsens | Now What?

Learn how the Federal Reserve expects to tame inflation and why homeowners and homebuyers should be concerned.

FIRST A REALITY CHECK

No one should view the July 13, 2022, inflation announcement (see Ex. 1) with any surprise or that the United States is in a worse position than it was a month ago. That announcement, however, was like a canary in a coal mine.

Ex. 1 - U.S. Inflation (CPI) Trends | Jan-1982 - Jun-2022

Folks, in previous blogs and newsletters, we discussed why inflation, and its companion side effects (higher interest rates, recession, rising unemployment and a devaluation of traditional asset classes) has arrived. Indeed, inflation and its negative side effects are likely to create economic and financial hardship for millions of U.S. individuals and businesses for many months if not years to come.

"Inflation is a dangerous disease for a society. It is a disease if allowed to go on unchecked can destroy a society.”

Milton Friedman, Economist

HOW DID WE GET HERE?

Few, if any of us, like to admit responsibility for the mistakes we made. That statement is no less true for politicians (both parties) or members of the Federal Reserve Board. The latter controls and is directly responsible for the management of the nation’s money supply, which if expansionary, can lead to periods of high inflation (see quote from Milton Friedman below).

“There is one and only one basic cause of inflation: too high a rate of growth in the quantity of money — too much money chasing the available supply of goods and services.”

Milton Friedman, Newsweek Magazine, Oct. 1977

The former, principally Congress, is responsible for the explosive growth in Federal spending and the nation’s ever increasing budget deficits (see Ex. 2) particularly during the COVID years.

Ex. 2 - U.S. Annual Budget Surplus (Deficit)

Since the U.S. budget, like all budgets, must balance (receipts = expenditures), the government has to fund any deficit through borrowings or the creation of money. This, of course, places a significant amount of political and other pressure on the Federal Reserve to create money so it can help congress fund its obligations.

This was particularly true during the COVID years when the Federal Reserve adopted a highly accommodative monetary policy which made it less expensive for people, businesses and the government to borrow and spend money. The net result was a dramatic increase in the growth of the U.S. money supply (see Ex. 3), which many economists recognize to be the root cause of inflation. Note there is typically a one-to-two-year lag between the growth in money supply and inflation.

Ex. 3 - U.S. Money Supply (M2) Growth Vs. Inflation (CPI)

NOW WHAT?

That’s the question the Federal Reserve’s Open Market Committee (FOMC) must answer when it meets next week (July 26-27) to discuss.

“We expect the Federal Reserve to raise its key policy interest rate (the federal funds rate) by at least 75 basis points if not a full percentage point (100 basis points) at this upcoming meeting.”

In our opinion, the FOMC is between a rock and hard place. They simply waited too long to address the inflation issue, which arguably they played a role in creating.

If they raise interest rates too aggressively then they risk killing the golden goose (U.S. GDP growth) which is already showing signs of recession (see section on Risk Implications | First Recession Then Unemployment). If they raise rates too slowly, then they risk inflation getting much worse than it already is, which could further destabilize the financial markets (see Section on Risk Implications | Real Estate and Other Asset Classes) and the employment situation (see Ex. 4). That’s the problem with inflation – The cure is often worse than the illness.

Ex. 4 - U.S. Unemployment Rate (%)

That said, it’s our view that the FOMC will persuade themselves that it is better to raise rates more significantly now versus later in the year when economic conditions will likely be worse. Moreover, we are assuming that the FOMC will take comfort in the fact that unemployment (see Ex. 4) is still at historically low levels, which is consistent with the Federal Reserve’s mandate of maximum employment. All told, that’s why we expect the FOMC to increase the federal funds rate by 100 basis points (1%) versus the 75 basis points they raised rates in June-2022 (see Ex. 5).

Ex. 5 - Federal Reserve Interest Rate Hikes in 2022

(Rate = Federal Funds Rate)

| DATE | RATE CHANGE (BASIS POINTS) |

|---|---|

| Mar-2022 (Actual) | 25 |

| May-2022 (Actual) | 50 |

| Jun-2022 (Actual) | 75 |

| Jul-2022 (Estimate) | 75-100 |

RISK IMPLICATIONS | FIRST RECESSION AND THEN UNEMPLOYMENT

Two side-effects of inflation is that it 1) increases the likelihood of an economic slowdown (i.e., recession) and 2) generally leads to higher unemployment.

Inflation, defined as a general increase in the cost of all goods and services in an economy, decreases the purchasing power of money for individuals and businesses alike. Consumers buy less goods and services because they can’t afford the same quantities. Businesses lower production levels to coincide with the lower level of demand. This usually results in employee layoffs as businesses need less labor to fulfill lower production levels. This, of course, results in an economic slowdown which if material can lead to a recession.

Recession | Here We Go Again

Many analysts and businesspeople are reluctant to utter the word “recession” because officially a recession doesn’t occur until you have two consecutive quarters of negative gross domestic product (GDP) growth and because nobody wants to think the unthinkable.

"The United States is already in the early stages of a recession. We don't need to follow some arbitrary, made-up definition to tell us what we can plainly see."

Folks, the United States is already in the early stages of a recession. We don’t need to follow some arbitrary, made-up definition to tell us what we can plainly see. Even the GDPNOW running estimate (unofficial of course) presented on the Federal Reserve Bank of Atlanta’s website indicates that GDP growth was -1.5% as of July 15, 2022. If accurate, that would meet the requirement of two consecutive quarters of negative GDP growth. Note GDP growth was -1.6% in the first quarter of 2022.

For individuals and families (working or retired), the determination of whether the country is in a recession or not is much simpler. First, if I want or need to work, can I find a good paying job? Secondly, how much disposable income will I have after I pay for necessary items such as food, energy, and shelter?

Unfortunately, the answer to the first question isn’t very good as many U.S. businesses are in the process of reevaluating and revising downward their 2022 and 2023 estimates for revenues and earnings. In fact, many businesses have already started, albeit incrementally, to announce layoffs, hiring freezes and, in some case, rescind job offers given the expected slowdown in economic activity. We expect this trend to accelerate with announcements of major layoffs coming as early as the third quarter of 2022.

As respects the second question, the answer, unfortunately isn’t any better. With an annual inflation rate of 9.1% (all items), most working-class individuals and families are already feeling the financial pinch. Interestingly or maybe frighteningly, the actual unofficial inflation number, according to ShadowStats is significantly higher. Note ShadowStats estimate of inflation uses what they call an alternate corrected version of the CPI calculation.

RISK IMPLICATIONS | REAL ESTATE AND OTHER ASSET CLASSES

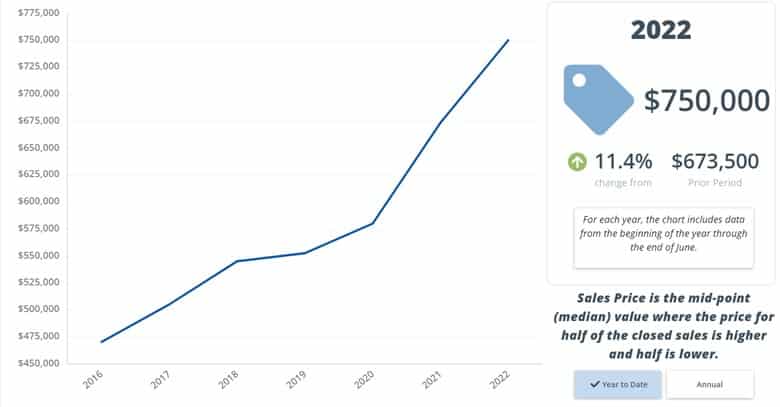

In the first half of 2022, prices of single-family homes in the greater Boston region improved considerably (11.4%) as compared to a year ago (see Ex. 6).

Ex. 6 - Sales Price | Greater Boston Region (YTD June 2022)

“Inflation and rising interest rates are causing affordability issues for homebuyers, which oddly enough, may correct the supply demand imbalance in housing which currently favors the seller. Any correction, however, is unlikely to improve the supply side of the equation but instead reduce demand.”

Real estate is one of the few asset classes that generally performs well in an inflationary environment (see Team Coyle’s Jan-2022 newsletter). That’s because historically real estate has proven to be an effective hedge against inflation, outperforming other asset classes (stocks, bonds, gold – See Ex. 7).

So far this year, that prediction has proven to be correct. However, as we noted in subsequent newsletters, periods of high and sustained inflation typically produce negative side effects such as higher interest rates, recession, rising unemployment, and higher property taxes.

These side effects are creating affordability issues for both homebuyers and homeowners which may cause home price growth in 2023 to turn negative, especially if the Federal Reserve raises interest rates too much and too fast.

Exhibit 7 - ASSET RETURNS (YTD JUNE 30, 2022)

| Asset Class | YTD Return |

|---|---|

| S&P 5001 | -20.58% |

| Gold Futures1 | -2.41% |

| U.S. Corporate Bonds1 | -14.39% |

| Greater Boston Real Estate2 | 11.4% |

1 Source: Wall Street Journal Market Data

2 Source: MLSPIN, Domus Analytics.

Other asset classes (stocks, bonds gold, etc.), unfortunately, have not done so well in today’s inflationary environment (see Ex. 7). This is not a surprise when you consider how these assets performed in past inflationary periods. The real concern, particularly for equities, is how worse can it get, and will the Federal Reserve take its foot off the inflation brake if the market starts to free fall. If that were to occur, we would still have inflation as a problem so that’s not a particularly good solution. It looks like Ol’ Mr. Friedman was right – the cure is worse than the disease.

WRAPPING IT UP

As we mentioned in our introductory remarks, the July 2022 inflation report was not a surprise but a harbinger of bad news to come.

Excessive congressional spending aided by an overly accommodating monetary policy (quantitative easing, artificially low interest rates, etc.) has brought us to the precipice of an economic malaise. Some people, however, will argue that it was necessary for Washington DC to pursue such fiscally irresponsible polices because of the COVID pandemic. Others will argue the opposite.

Regardless of who’s right, we must now prepare ourselves for the inevitable malaise of higher interest rates, recession, rising unemployment, and a devaluation of traditional asset classes. How bad conditions get will depend on the policies adopted. Hopefully, our policymakers (both sides of the aisle) in Washington can learn from their mistakes – like don’t try and micromanage the economy and stop the ridiculous amount of spending. But then again, maybe they won’t.

Disclaimer: The views and opinions expressed in this commentary reflect Team Coyle’s beliefs and observations as of the date of publication. Team Coyle undertakes no responsibility to advise you of any changes in the views expressed herein. No representations are made as to the accuracy of such observations and assumptions and there can be no assurances that actual events will not differ materially from those assumed. The forward-looking statements in this paper are based on Team Coyle’s current expectations, estimates, forecasts and projections, and are not guarantees of future performance. Actual results may differ materially from those expressed in these forward-looking statements, and you should not place undue reliance on any such statements. These materials are provided for informational purposes only, and under no circumstances may any information contained herein be construed as investment advice. See also terms of use.

About TEAM COYLE

Team Coyle, a professional group of real estate agents at Compass, has more than ten years of experience helping individuals and families buy and sell real estate in the Greater Boston Region of Massachusetts (primarily MetroWest).